Quadrennial events drive a $5bn uplift in 2026, but structural changes in ownership, distribution and regulation suggest a more complex future for sports media

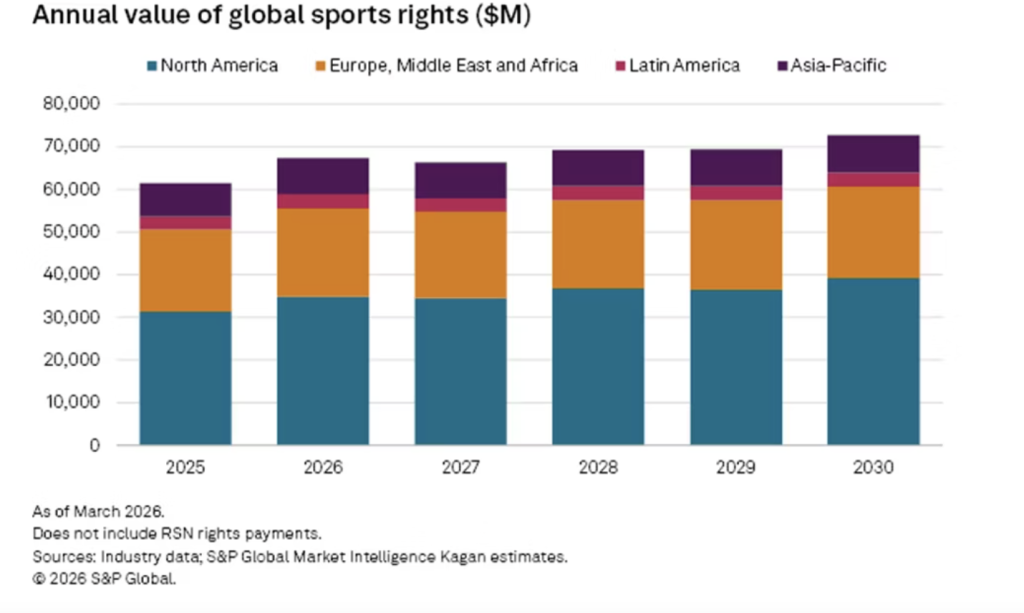

Global sports media rights spending will reach $67.34bn in 2026, according to new analysis from S&P Global, but the headline growth masks a deeper shift in how sport is financed, distributed and consumed.

The 9.6% year-on-year increase is largely driven by the calendar rather than by a fundamental acceleration in underlying demand. Two major events – the FIFA World Cup 2026 and the Winter Olympics – are expected to account for the bulk of a $5bn uplift, with the expanded World Cup alone projected to generate around $4bn in media revenue.

This concentration raises questions about how sustainable current growth levels are outside of peak event cycles, particularly as rights values continue to climb across domestic leagues.

North America remains the centre of gravity. The region will account for 52% of global sports media rights spend in 2026, equating to $34.9bn, with the US contributing $32.8bn. Rights valuations in the region are forecast to grow by 11% year-on-year, underlining the continued pricing power of US sports leagues.

Yet the more telling development may not be the scale of spending, but the evolving relationship between rights holders and broadcasters.

In January, the NFL finalised a landmark agreement with The Walt Disney Company that included taking a 10% equity stake in ESPN. The move signals a shift away from traditional buyer-seller dynamics towards deeper strategic alignment between leagues and media companies.

This model is emerging alongside a wave of consolidation and restructuring across the media landscape. The combination of Warner Bros. Discovery and Paramount Global’s Skydance-backed assets, as well as the creation of new sports-focused divisions, reflects how central live sports media rights have become to broader M&A strategies.

Streaming platforms are also continuing to reshape the market. Companies such as Amazon have increased investment in live sports as a means of driving subscriptions, while traditional broadcasters face ongoing margin pressure from cord-cutting.

However, this shift is not without consequence. As rights fragment across multiple platforms, consumers are increasingly required to subscribe to several services to follow a single sport or competition. The growing cost burden has prompted scrutiny from the Federal Communications Commission, which has launched inquiries into the migration of sports content away from linear television.

At a local level, the breakdown of regional sports networks has forced leagues to rethink distribution models. Major League Baseball has begun rolling out team-specific channels to replace traditional RSN coverage, while the National Basketball Association is exploring the creation of a national streaming model for local sports media rights.

How sport is packaged has changed

These shifts are also feeding into broader changes in how sport is packaged and monetised. Growth in “non-event” programming, from documentaries to shoulder content, is creating new inventory for rights holders, while expanding their reach beyond live broadcasts.

At the same time, the convergence between sports media and betting continues to accelerate. Legal operators such as FanDuel and DraftKings are now competing not only with each other but with prediction market platforms like Polymarket, which offer peer-to-peer wagering models that sit outside traditional regulatory frameworks.

Taken together, the data points to a market that is still growing, but becoming more complex and, in some cases, more fragile. While live sport remains one of the few forms of content capable of consistently drawing mass audiences, the systems that underpin its distribution are being reworked in real time.