The Beckham-backed organisation that once floated with a £41.2m valuation has ceased operations after an insolvency sale failed to find a buyer. What does its rise-and-fall say about esports as a public-markets bet?

Guild Esports launched in 2020 with a simple, headline-friendly proposition: bring Premier League polish to competitive gaming, and finance it like a modern sports property.

The company raised £20m ahead of its London Stock Exchange debut and listed on October 5, 2020 with a market capitalisation of about £41.2m, becoming the first esports organisation admitted to the LSE.

Later, through his image-rights vehicle, ex-England footballer David Beckham took a small equity stake and signed a five-year ambassador agreement that guaranteed multi-million-pound marketing payments tied to merchandising and sponsorship, later pared back in 2022.

It helped open doors for sponsors and investors, but it also added fixed costs during the scale-up years.

The early playbook was sponsorship-led growth plus brand building. A multi-year partnership with Sky gave Guild naming rights at its Shoreditch HQ – rebranded the Sky Guild Gaming Centre – and underlined its ambition to be a mainstream-ready platform for partners.

Yet the public numbers told a tougher story. Guild’s 2023/24 annual results (published January 31, 2024) showed revenues up 24% to £5.53m and gross profit up 44% to £3.99m, lifting gross margin to 72%.

Administrative expenses fell to £7.40m from £10.91m and the pre-tax loss narrowed to £4.50m. Liquidity remained tight, however.

Cash as of September 30, 2023 was £0.46m, operating cash outflow for the year was £2.06m, and the balance sheet showed negative equity of £0.23m with net current liabilities of about £1.88m, despite a reported £5m order book to be recognised over contract lifetimes. Management flagged the potential need for a fundraising in the year ahead.

The June 28, 2024 interim update underlined that pressure. First-half revenue fell to £2.1m from £3.7m, largely because H1 2023 benefited from a one-off £1m Fortnite prize that is mostly paid through to players.

Loss before tax improved to £1.8m from £2.28m after a 38% cut in admin costs to £2.65m, and the revenue mix shifted, with Guild Studios contributing £586k (up 537% year on year), sponsorship £1.12m and prize money £270k. Cash at 31 March 2024 was just £17k, rising to £110k by 25 June, and the going-concern note acknowledged a “material uncertainty.”

By mid-2024 the liquidity squeeze forced a formal strategic review and on August 1 the company disclosed a cash position of £25,000, confirmed liabilities of £1.36m falling due by the end of September, and £1.52m of receivables.

In October 2024, US investor DCB Sports acquired 100% of Guild’s operating assets for a £100,000 cash payment and the assumption of more than £2m of liabilities. Operations moved into a new private company, Guild Esports & Gaming Ltd, while the listed shell continued separately.

It was a clear reset, but also confirmation that the original public-markets bet had failed to meet expectations.

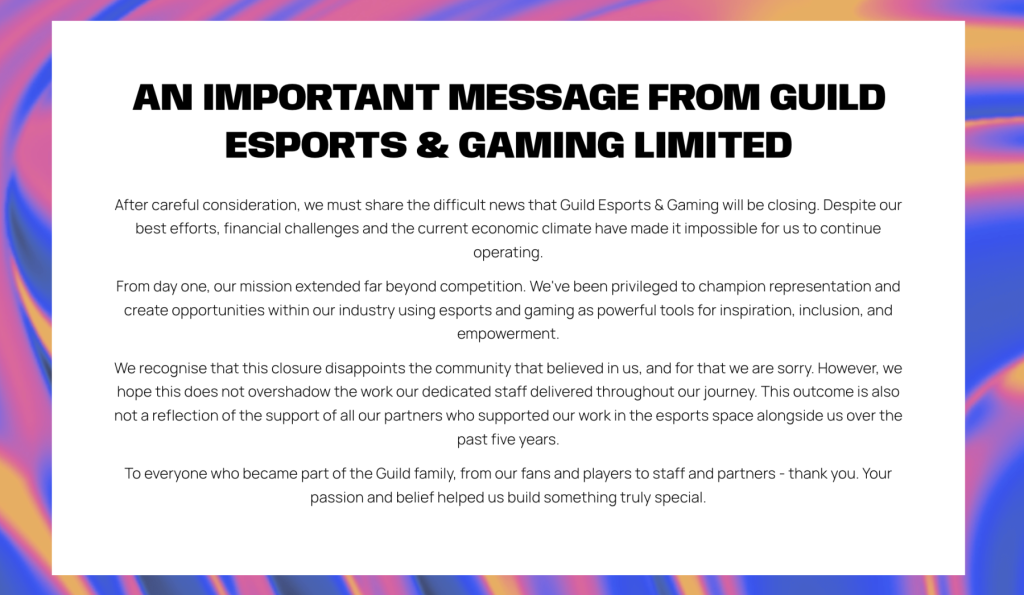

The reset didn’t stick. On August 14, 2025, reports surfaced that Guild had been put up for sale on an insolvency marketplace with bids due the next day. A week later, on August 21, Guild announced it would cease operations, citing “financial challenges” and the economic climate.

Multiple outlets, and Guild’s own social post, confirmed the closure.

What the rise-and-fall signals

Public markets proved an unforgiving place for an esports start-up. Guild’s IPO was a milestone for the UK scene, but the discipline of quarterly scrutiny demands predictable cash flow. The company’s model leaned on sponsorship, tournament-linked prize money and audiences that rise and fall with the game cycle, all of which are hard to forecast without diversified media rights or revenue sharing from publishers.

That fragility surfaced in the numbers. Guild’s filings repeatedly showed a widening gap between brand income and the cost of running teams, talent and content.

High-profile partnerships could not bridge that gap. The Sky agreement delivered credibility and inventory, yet the financial trajectory still pointed towards losses, and investors ultimately looked past celebrity backing and marquee logos to the underlying unit economics.

The 2024 rescue by DCB Sports bought time by taking on liabilities and keeping operations going, but it did not change the fundamentals: without a step-change in revenue quality or the cost base, the insolvency risk quickly returned and the story ran out of road.

Guild was an ambitious test case: could a UK esports organisation behave – and be valued – like a listed sports-media business?

The answer, at least this cycle, was no. From a £41m flotation in 2020 to a closure announcement on August 21, 2025, the journey maps the wider recalibration of esports economics.