PwC’s latest Global Sports Survey found sports executives increasingly expect sponsorship, hospitality and digital engagement revenues to outpace media rights growth, as younger audiences continue shifting toward creator-led and short-form content consumption.

For years, the global sports industry has operated on a relatively simple assumption: live broadcasting rights would continue rising in value, underpinning almost every other commercial ambition around them.

But while stadium districts expand into year-round real estate ecosystems, creator-led leagues chase younger audiences on TikTok and YouTube, and investors pour money into emerging sports properties, one of the more striking findings in PwC’s latest Global Sports Survey is that executives increasingly believe the old engine of growth is beginning to slow.

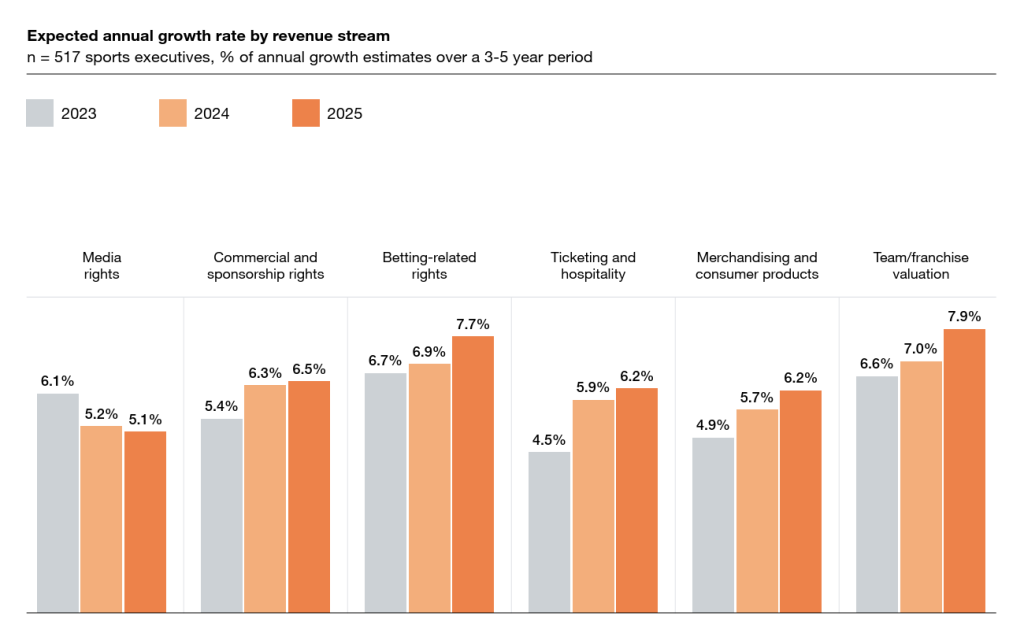

According to the consultancy’s ninth annual report, sports executives now expect media rights growth to lag behind sponsorship, betting-related rights, ticketing and hospitality growth over the next three to five years.

The report, based on responses from 517 senior sports executives across 48 countries and a parallel fan survey of 7,250 respondents across 17 countries, paints a picture of an industry still expecting strong growth, but increasingly searching for it elsewhere.

PwC found executives expect overall annual sports industry growth of 7.4% over the next three to five years, down from an estimated 8.5% growth over the previous period. Asia is expected to remain the fastest-growing region at 9.4%, followed by North America at 8.5%, while Europe is forecast at 6.7%.

Yet behind those headline growth figures sits a more complicated reality: sports organisations increasingly appear to be repositioning themselves less as traditional rights holders and more as broader entertainment, infrastructure and digital media businesses.

The media rights model begins to fragment

One of the report’s most interesting findings is the growing concern around media rights growth.

Executives surveyed by PwC forecast annual media rights growth of 5.4% over the next three to five years, below every major revenue category except merchandising. Sponsorship rights are expected to grow at 6.9%, betting-related rights at 7.7%, while ticketing and hospitality are projected at 6.7%. Team and franchise valuations are forecast to rise by 7.9%.

PwC said the slowdown reflects increasing divergence between premium and non-premium properties, alongside broader fragmentation across viewing habits and distribution platforms.

“While media rights remain critical, slower growth in this segment underscores the importance of diversified revenue streams in sustaining the overall market expansion,” the report stated.

The survey suggests many executives now see sponsorship, hospitality, direct-to-consumer engagement and experiential revenue as increasingly important counterbalances to softer broadcast growth. This shift is also influencing investment behaviour. PwC found 78% of executives expect investors to prioritise sports assets with diversified revenue streams beyond traditional media rights over the next three to five years.

Examples highlighted in the report include properties such as PTO’s T100 triathlon series, Hyrox, creator-led competitions like Kings League, as well as women’s leagues and fight sports. PwC argues these models are attractive because they combine media, sponsorship, participation fees, memberships and digital commerce into broader commercial ecosystems.

David Rader, President and COO of UNA Sports Group, argued that despite changing formats and technology shifts, ownership of premium intellectual property remains central to long-term value.

“Teams and leagues are the economic engines of this industry,” he said within the report. “They control the intellectual property, the scarcity, and the cultural relevance that drive enduring value.”

However, the survey also reveals a tension emerging between investor appetite and fan behaviour. While 55% of executives believe investment capital will favour emerging or breakaway sports models, 63% of fans surveyed still said they preferred traditional leagues and structures.

Younger fans are changing how sport is consumed

If the report has a defining theme, it is the growing fragmentation of fandom.

Among fans aged 18-24, 58% said they consume sports highlights through social media platforms such as TikTok and Instagram, while 25% engage with athlete-led content and 21% consume creator-led sports content. Gaming experiences also featured heavily among younger demographics.

Older audiences remain far more concentrated around traditional broadcasts, with 78% of respondents aged over 65 primarily consuming live sports through official television or streaming channels.

The report argues that rights holders can no longer rely on a single distribution model. Jo Redfern, an executive producer specialising in youth-focused digital media strategy, said younger audiences increasingly view live broadcasts as only one component of a wider content ecosystem.

“Live content, historically the central pillar of a sport’s business model, still holds a place of importance, but its primacy is diminishing among younger demographics,” she said.

She added that creator commentary, short-form clips and participatory digital experiences were becoming increasingly important alongside traditional live coverage.

“What was once a vertical model anchored in broadcast is evolving into a more distributed ecosystem in which content is spread, shared and reinterpreted across multiple touchpoints,” Redfern said.

The survey suggests many sports organisations are still attempting to work out how to balance traditional broadcast revenues with the growing need for accessibility across social and digital platforms.

PwC found that teams and clubs are moving faster toward digital-first strategies than leagues, partly because long-term media rights agreements continue to underpin league economics. At the same time, executives acknowledged that monetisation becomes more difficult as audiences fragment across platforms where advertising yields and subscription models are less established.

Women’s sport enters a new commercial phase

Women’s sport remains one of the strongest growth stories in the report, though the findings also suggest the industry may be moving into a more challenging stage of commercial development. PwC found 91% of executives expect double-digit revenue growth for women’s sport over the next three to five years.

North America is expected to lead much of that growth, driven by properties such as the WNBA and NWSL, while Europe’s momentum continues to centre heavily around football.

However, the survey also indicates monetisation remains uneven. Only 22% of fans said they were as willing to pay for women’s sports content as they were for men’s sports, while 44% said they were not willing to pay for women’s sports content or events.

PwC concluded that women’s sport remains in what it described as a “reach-over-revenue stage”, where audience growth and visibility remain more important than direct subscription monetisation.

The report also notes that investment in women’s sport is increasingly being driven by long-term strategic positioning rather than short-term returns. Bex Smith, Founder and CEO of Crux Football, argued that much of Europe’s women’s sports ecosystem is still being built.

“The women’s game is still in an investment phase,” she said. “Returns will come, but only if investors understand they are helping build an industry, not just buying into a mature one.”

Holly Murdoch, COO of WSL Football, similarly described women’s sport as being in the early stages of broader structural transformation.

“Women’s football is a new sport within a very established industry,” she said. “Like any growing business, it needs upfront investment to supercharge its progress.”

Stadiums become year-round commercial districts

Away from media and fandom, the report also highlights how sports venues themselves are increasingly evolving into broader mixed-use developments.

PwC argues that stadiums are no longer being designed solely around matchdays, but increasingly as anchors for residential, hospitality, retail and entertainment districts capable of generating revenue throughout the year.

Jonathan Fascitelli, Founder and Chairman of Seregh and former CEO of Harris Blitzer Sports & Entertainment Real Estate, said the “real upside” increasingly sits outside the stadium itself.

“Transforming a stadium from a 15-day asset into a 365-day hub creates new economic engines that benefit teams, cities, and communities,” he said.

PwC predicts at least half of major league teams will eventually operate within some form of mixed-use district.

Interestingly, however, the report also identifies a disconnect between executives and fans when it comes to matchday priorities. While executives tend to focus on food, beverage and immersive technology upgrades, fans ranked cleanliness, seating comfort, ticket affordability and restroom access among the most important drivers of stadium satisfaction.

The consultancy concluded operators should prioritise “fundamentals before layering luxury”.

Integrity and trust move higher up the agenda

The report’s final section focuses on integrity, which executives increasingly see as a direct commercial issue rather than solely a governance matter. Three-quarters of respondents said integrity breaches represented one of the biggest commercial risks facing sport.

Match-fixing and game manipulation ranked as the biggest integrity threats, followed by doping and financial misconduct.

Alex McLin, Unit Lead of FIFA Foundation’s independent Safe Football Support Unit, said integrity concerns have moved from the margins of sports governance into mainstream strategic discussions.

“Ten years ago, integrity was often treated as a compliance requirement, something to be acknowledged but rarely championed,” he said. “Today, there is greater awareness, more dedicated integrity units, and a broader understanding of what integrity truly means in sport.”

For all the optimism around sports growth, digital engagement and new commercial formats, PwC’s report ultimately paints a picture of an industry in transition.

The sports business is still expanding. But increasingly, the growth is expected to come from creator ecosystems, sponsorship diversification, digital engagement, hospitality, real estate and direct fan relationships, rather than relying solely on ever-rising broadcast deals.