The women’s game has reached a new commercial milestone, but Deloitte’s latest Football Money League suggests revenue growth alone is no guarantee of structural stability.

Jennifer Haskel, knowledge and insights lead in the Deloitte Sports Business Group, will be at Stamford Bridge this weekend, taking her usual seat for women’s Arsenal vs Chelsea – a fixture that increasingly feels like the centre of gravity in the women’s game.

She laughs that she lives “right around the corner”, but the truth is she’d be there regardless. “I’m a massive women’s football fan,” she says. “I’ll be at the Arsenal Chelsea game this weekend.”

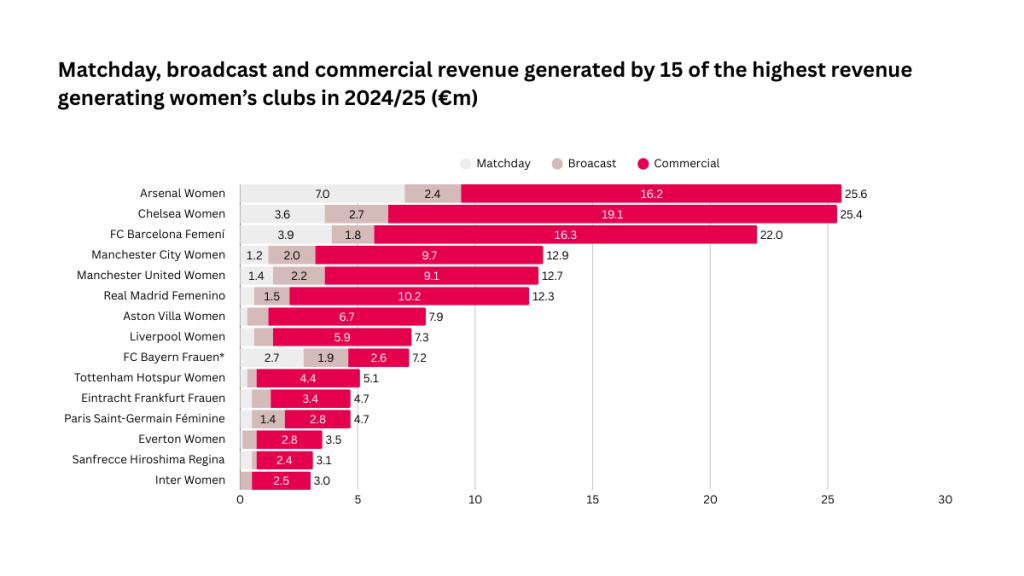

It’s a fitting backdrop for the release of Deloitte’s latest Football Money League (Women’s), which shows the sport hitting a symbolic milestone: the top 15 revenue‑generating clubs have surpassed €158m for the first time, growing 35% year‑on‑year for the second season running. The numbers are impressive but they also raise a more complicated question.

If women’s football is accelerating this quickly, is it finally moving beyond its proof of concept era, or is it still very much a start‑up industry with a few scaled leaders?

A top‑heavy surge — and why Deloitte isn’t worried

The headline finding is hard to ignore: Arsenal Women (€25.6m), Chelsea Women (€25.4m) and FC Barcelona Femení (€22m) now account for almost half of all revenue in the top 15. The gap between the elite and the rest is widening.

But Haskel is quick to push back on the idea that this concentration is a red flag. “I don’t think polarisation is specific to the women’s game,” she says. “We see it across the men’s game as well.” Her hope is that the investment made by the top three becomes “the rising tide that lifts all boats”.

The report also makes clear there is no single blueprint for success. Arsenal’s long‑standing ‘one‑club’ model contrasts sharply with Chelsea’s carve‑out, which now operates with dedicated leadership and its own commercial strategy. Both approaches are working, and both are attracting brands.

* FC Bayern Frauen’s matchday revenue also includes revenue from participation in the World Sevens competition. This income has been classified as Broadcast for other clubs included in our analysis. Additionally, the club’s commercial revenue may include revenue attributable to transfer-related income. This income is not included in the revenue of any other clubs included in our analysis.

On‑pitch performance still matters too. “The top three all won significant trophies,” Haskel notes, and this success brings “new fans, new followers, and brand equity” that feeds directly into commercial growth.

For all the momentum, she is adamant the sport remains in its early stages. Many leagues are only now setting minimum professional standards or moving towards independent governance. “We still are in that start‑up phase,” she says. “What that requires is investment — not just capital, but infrastructure, time, effort, volunteers… we’re still in the early days of figuring out what those structures need to be.”

Commercial power, matchday innovation and the broadcast lag

If there is one clear engine of growth, it’s commercial revenue. Deloitte finds it now accounts for 72% of income among the top 15 clubs; a sign of both brand appetite and the underdevelopment of other revenue streams.

Haskel believes the commercial ceiling is still far from reached. “We’re just scratching the surface,” she says, pointing to the rise of “authentic and organic partnerships” across the pyramid. Crucially, she notes clubs are finally seeing better attribution from club‑wide deals: “We’re starting to see a lot more attribution to the women’s side… through social media engagements” and other non‑traditional metrics.

Matchday revenue is also rising, but attendances have dipped for several Women’s Super League (WSL) clubs. This contradiction reflects a deeper challenge: women’s football fandom behaves differently. “Women’s football fans are a bit more fluid than traditional men’s football fans,” Haskel explains. Clubs need to “work a little bit harder” to create the kind of experience that builds loyalty and repeat attendance. The positive feedback loop – go once, enjoy it, return – is not yet guaranteed.

Broadcast revenue remains the weakest link. It fell proportionally to 13% of total income, partly due to rights‑cycle timing, but also because the industry still hasn’t figured out how to measure women’s sport consumption.

“It might not be the traditional viewership figures,” Haskel says. “There’s a lot of Instagram engagement.” The challenge is turning that visibility into value.

She also warns against overloading the calendar in pursuit of broadcast uplift. “We want to drive revenue, but not at the expense of player injuries,” she says, a reminder that the women’s game cannot simply replicate the men’s model.

The shift to sustainability – and what maturity will really look like

If there is one indicator Haskel sees as the clearest sign of the sport transitioning into an established commercial phase, it’s not revenue. It’s staffing.

“You have to have some type of dedicated resource,” she says. Too often, women’s teams have relied on people juggling responsibilities — “a side‑of‑desk project”, as she puts it. The clubs climbing the rankings are the ones with dedicated commercial leads, ticketing teams, and leadership structures built specifically for the women’s game.

This shift is happening at league level too; the WSL’s move to independence, the Frauen‑Bundesliga’s breakaway from the DfB, and club carve‑outs at Chelsea and Aston Villa all point to a sport taking control of its own destiny. Investment funds (from Blue Owl to Monarch Collective) are circling with a mix of commercial ambition and mission‑driven purpose.

The next five years will determine whether the sport can convert rapid growth into long‑term stability. Haskel believes the potential is enormous, but only if stakeholders resist the temptation to rush. “We’re still in the early days,” she says. “We have to create the environment we want to see.”